FLA Return Filing with RBI under FEMA

The FLA Return is the annual statement of foreign assets and liabilities that every Indian entity holding FDI or ODI must file with the RBI by 15 July. Our specialists confirm your applicability, prepare and submit the return on the FLAIR portal, and revise it on audited figures.

🗹 FLA Returns Under FEMA – A Brief Overview |

||

|---|---|---|

| 1 | What is the FLA Return? | The annual RBI return of an Indian entity’s outstanding foreign assets and liabilities, FDI received and ODI made as on 31 March, under FEMA, 1999. |

| 2 | Who must file | Indian companies, LLPs, AIFs, partnership firms and PPPs holding outstanding FDI or ODI as on 31 March (even with no fresh activity during the year) |

| 3 | Where it is filed | Online on the RBI’s FLAIR portal (flair.rbi.org.in); there is no government fee to file. |

| 4 | Documents needed | Entity CIN and PAN, the authorised person’s PAN, the Authority and Verification letters, and your 31 March financials with FDI/ODI details. |

| 5 | Due Date | 15 July every year, on provisional figures; revised on audited accounts by 30 September. |

| 6 | Late Fee | A flat Late Submission Fee of ₹7,500 per return regularises a simple delay; compounding applies only where the LSF route does not. |

| 7 | Linked filing | Entities and resident individuals with ODI also file the Annual Performance Report (APR) by 31 December. |

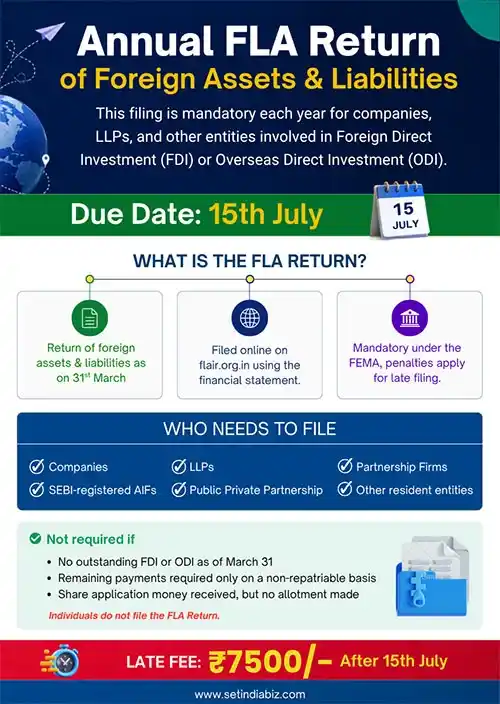

What is the FLA Return?

The Annual Return on Foreign Liabilities and Assets (FLA Return) is a mandatory annual filing under the Foreign Exchange Management Act, 1999, first notified by A.P. (DIR Series) Circular No. 45 dated 15 March 2011. The FLA Return is a position-based filing that captures an entity’s outstanding stock of foreign investment (inward FDI and outward ODI) as of 31 March annually, supporting the RBI’s International Investment Position data.

Filing is now done online on the RBI’s FLAIR portal (flair.rbi.org.in), which replaced the earlier email-and-Excel system as of 28 June 2019. Setindiabiz specialists assess whether the obligation applies to you, register your entity on FLAIR, prepare the return across all five sections, file it by the due date, and submit the revised return once your accounts are audited.

Pradeep Vallat

Founder "Autonomo""Setindiabiz’s knowledgeable, disciplined, and organized team made our company registration, tax, and IPR filings smooth, hassle-free, and worry-free."

Who Must File the FLA Return

The FLA Return follows the foreign investment on your balance sheet, not your activity during the year. The obligation rests on the Indian entity and is triggered the moment any outstanding FDI or ODI exists as on 31 March — even if no money came in or went out that year, even if the foreign investor is dormant, and even where the foreign holding is indirect. Under FEMA, 1999, the entity itself is responsible for the filing, not the foreign investor or individual shareholder.

Indian Company

Indian companies within the meaning of Section 1(4) of the Companies Act, 2013, that have received FDI or made ODI and carry it on their books as on 31 March.

Indian LLP

LLPs registered under the Limited Liability Partnership Act, 2008, that have received foreign capital contributions or made overseas investments.

Partnership Firms

Partnership firms that have received FDI or made ODI; the RBI issues a dummy CIN on request, used only for FLA filing.

SEBI Registered AIF

Alternative Investment Funds file, using the latest Excel format, to be emailed to flareturn@rbi.org.in after registering on FLAIR, not through the online form.

Public-Private Partnerships

PPPs that hold outstanding foreign assets or liabilities as on 31 March.

Other Resident Entities

Any other Indian-resident entity holding outstanding foreign assets or liabilities (for example, trusts and the Indian offices of foreign entities); a dummy CIN is issued where the entity has no CIN.

Important Note: An entity that received FDI in any earlier year must keep filing every July until that investment is fully divested; indirect or downstream foreign holding (where a non-resident holds through another Indian entity) is still foreign investment and must be reported; and an entity that has made ODI must file the FLA Return and the separate Annual Performance Report (APR), due 31 December, monitored by a different RBI department.

Milestones of FLA Filing

Applicability Check

Applicability check and FLAIR registration (first-time filers) or login retrieval.

Data Compilation

Compilation of financial and FDI/ODI data, and drafting of the Authority and Verification letters.

FLA Return Filing

Provisional FLA Return prepared and submitted on FLAIR; acknowledgement received.

FLA Revision

Revised FLA Return filed on audited accounts, where provisional figures were used.

Turnaround for the filing itself is typically 2–4 working days from receipt of complete data; the 30 September revision is calendar-driven, not effort-driven.

Process of FLA Return Filing on the FLAIR Portal

FLA return filing is a FEMA reporting obligation that is completed entirely online via the RBI’s FLAIR portal. Before starting, the entity appoints an authorised person by way of a Letter of Authority on its letterhead, signed by an appropriate officer. It prepares the Verification Letter in the prescribed format. The steps below follow the full route (from first-time registration through to acknowledgement; entities already registered simply log in and skip Step 1).

Step 01: Register the entity on FLAIR

We create your Business User account on flair.rbi.org.in, entering the entity and authorised-person details and uploading the Authority and Verification letters in the prescribed formats. Once we submit, the RBI emails the login credentials to your registered email.

🕒 Turnaround: 1–2 working days, subject to RBI credential issue.

Step 02: Log in and open the FLA form

We sign in with the credentials and the email OTP, change the first password, and open the online FLA return form from the home page.

🕒 Turnaround: same day.

Step 03: Prepare and submit the return

We complete Sections I to IV — identification, financial details, foreign liabilities and foreign assets — reconciled to your 31 March position, confirm the auto-generated Section V Variation Report, and submit. We file with provisional figures when your accounts have not yet been audited.

🕒 Turnaround: 1–2 working days from receipt of complete data.

Step 04: Acknowledgement and revision

Upon submission, the portal displays a system-generated acknowledgement, which serves as the official receipt. Where provisional figures were filed, we submit the revised return on audited accounts by 30 September.

🕒 Turnaround: acknowledgement on submission; revision by 30 September.

Why businesses trust us

⚖️ Due Date, Late Filing, Penalty and Compounding

The FLA Return is due annually by 15 July and reflects the entity’s position as of 31 March. If audits are pending, file with provisional figures by the July deadline and submit a revised return on audited data by 30 September. Delaying the filing is a FEMA contravention; however, the law provides an LSF route for simple delays and a stricter compounding process for unaddressed defaults.

Regularising a simple delay by paying LSF (the Late Submission Fee)

Late FLA Returns are regularised by paying a flat Late Submission Fee (LSF) of ₹7,500 per return. Under A.P. (DIR Series) Circular No. 16 (2022), this voluntary alternative to compounding allows the RBI to condone delays. A conditional acknowledgement is issued upon filing, with the final receipt provided after payment. The LSF is available for up to three years from the due date, and the fee must be paid within 30 days of the advice.

| No | Item | Position |

|---|---|---|

| 1 | Due date |

|

| 2 | Government filing fee | NIL |

| 3 | Late Submission Fee | The Late Submission Fee (LSF) is a flat fee of ₹7,500 per return, applicable for delays of up to 3 years from the original due date. |

- The delay exceeds the three-year LSF eligibility window;

- The entity disputes the RBI’s LSF calculation and chooses adjudication;

- The issue involves substantive contraventions beyond mere reporting delays; or

- The RBI issues a Memorandum of Contraventions, or the entity fails to file/pay the LSF.

Adjudication under Section 13(1) of FEMA can result in penalties up to three times the amount involved, or ₹2,00,000 if unquantifiable, plus ₹5,000 per day for continuing defaults. Compounding requires regularising the underlying default, costs ₹10,000 plus GST, and is typically resolved within 180 days.

FLA vs Other FEMA Filings

Entities with foreign investment carry more than one FEMA filing, and the FLA Return is frequently confused with the event-based forms. The distinction is simple: the FLA Return reports a yearly stock position, while FC-GPR and FC-TRS report individual transactions, and the APR reports the performance of overseas investments. One filing does not substitute for another — an entity can have a mandatory FLA Return in a year with no fresh transactions at all.

| Filing | What it reports | When | Trigger |

|---|---|---|---|

| FLA Return | Outstanding stock of foreign assets and liabilities as on 31 March | 15 July (revised by 30 September) | Outstanding FDI/ODI on the balance sheet |

| FC-GPR | Issue of capital instruments to a non-resident | Within 30 days of allotment | A fresh share allotment to a foreign investor |

| FC-TRS | Transfer of capital instruments between resident and non-resident | Within 60 days of transfer | A secondary share transfer |

| APR | Performance of an overseas JV/WOS | 31 December | Having made ODI |

Frequently Asked Questions

It is the Annual Return on Foreign Liabilities and Assets, filed with the RBI under FEMA, 1999. It reports the outstanding stock of foreign assets and liabilities on an Indian entity’s balance sheet as on 31 March each year. It feeds the RBI’s compilation of India’s international investment position.

It is notified under FEMA, 1999, by A.P. (DIR Series) Circular No. 45 dated 15 March 2011, and reported under the Master Direction – Reporting under FEMA, 1999. Filing is now done online via the FLAIR portal, which replaced the email-and-Excel system as of 28 June 2019.

No. FC-GPR reports a fresh share issue to a non-resident, FC-TRS reports a share transfer, and the APR reports the performance of overseas investments. The FLA Return reports the yearly stock position. They are separate filings; an entity with ODI files both the FLA Return and the APR.

Any Indian company, LLP, SEBI-registered AIF, partnership firm or PPP that holds outstanding FDI or ODI as on 31 March. The obligation lies with the Indian entity, not with the foreign investor or individual shareholder.

Yes, if any FDI or ODI remains outstanding on your balance sheet as on 31 March. The return is triggered by the stock position, not by activity during the year, and dormant companies are not exempt.

No. The FLA Return applies to entities. Where a non-resident invests in an Indian company or LLP, the Indian entity files; the individual investor does not.

Entities with nil outstanding foreign assets/liabilities as on 31 March, entities that issued shares to non-residents only on a non-repatriable basis, those that received only share application money without allotment, and those where all non-resident shareholders have exited to residents during the year.

Yes. As long as the foreign investment remains outstanding on your books as on 31 March, the FLA Return is due every July until the investment is fully divested.

Online on the RBI’s FLAIR portal. The entity registers a Business User account, uploads the Authority and Verification letters in the prescribed formats, logs in with the credentials and OTP, completes the five sections, and submits to receive a system-generated acknowledgement.

Identification details, financial details (capital, reserves, profit, sales and purchases, employees), foreign liabilities (inward FDI, split at the 10% direct/portfolio test), foreign assets (outward ODI), and an auto-generated variation report comparing the year to the previous year.

Identification fields fill from your FLAIR registration, and the non-resident investor master list is pre-filled for repeat filers (editable via Edit/Delete). The Variation Report auto-compares the two years. First-time filers enter everything fresh.

Not directly. You must request the RBI to unlock that year on the portal (via the revised-FLA approval link, tracked under the Multiple Year Enable Screen) or email surveyfla@rbi.org.in. Once approved, you can modify or delete that year’s return and resubmit.

File on provisional figures by 15 July to stay within the due date, then submit the revised return on audited accounts by 30 September. Do not wait for the audit and miss the July date.

15 July every year for the provisional return, and 30 September for the revised return on audited accounts.

A flat Late Submission Fee (LSF) of ₹7,500 per return, under A.P. (DIR Series) Circular No. 16 dated 30 September 2022. It is a way to regularise a simple delay and is available up to three years from the due date.

No. The LSF is the route to avoid penalties for a simple delay, not an addition to them. The Section 13 penalties apply only where a contravention is adjudicated rather than regularised.

When the delay is beyond the three-year LSF window, when you decline the LSF and opt for adjudication, when the matter is more than a reporting delay, or when the RBI has issued a Memorandum of Contraventions. Compounding is under Section 15, FEMA, 1999, read with the Foreign Exchange (Compounding Proceedings) Rules, 2024.

Under Section 13(1), FEMA, 1999, up to thrice the sum involved, or up to ₹2,00,000 where the amount is not quantifiable, plus ₹5,000 per day for a continuing contravention.

The compounding application fee is ₹10,000 plus GST, and applications are disposed of within 180 days under the Foreign Exchange (Compounding Proceedings) Rules, 2024 and the RBI Direction dated 1 October 2024. The underlying default must be regularised first.

Yes. Our specialists assess applicability, register your entity on FLAIR, prepare and file the return, and submit the audited revision — and where a prior-year figure needs correcting, run the RBI approval route on the portal.

Setindiabiz is Trusted By Leading Brands